If you’ve ever found yourself digging through your wallet trying to figure out where that one paycheck went or wondering how to keep better track of your bills, chances are—it’s time for a checking account.

Whether you’re fresh out of college, moving to the U.S., or just never got around to opening one, the process isn’t as complicated as it might seem.

Let’s walk through it, step by step, with zero jargon and just enough detail to help you feel confident.

First Off, What Exactly Is a Checking Account?

Let’s break it down real quick. A checking account is what most people use for everyday money stuff—paying bills, buying groceries, getting your paycheck, withdrawing from ATMs, swiping a debit card, all of it.

Think of it as your money’s launchpad. You keep funds there for easy access. No frills, no high interest (usually), just practicality.

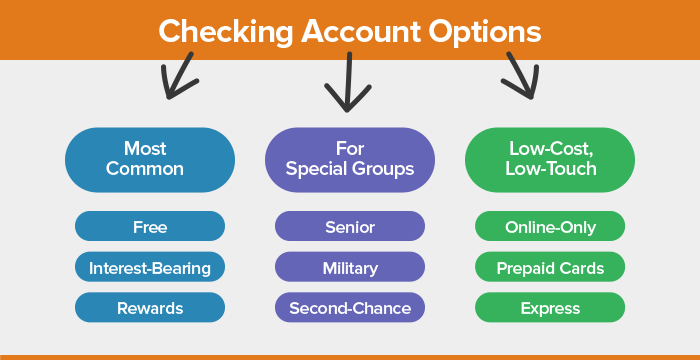

If you’re curious about the different kinds available—basic, interest-bearing, student, senior—you can check out more on account type checking. Why Do You Even Need One?

Sure, cash works—but carrying wads of bills is inconvenient, risky, and hard to track.

A checking account brings structure to your daily finances.. It lets you:

- Get paid via direct deposit

- Set up auto-pay for utilities, subscriptions, rent

- Use debit cards and ATMs

- Track where your money’s going

- FDIC-insured up to a certain limit, which is helpful if a bank fails

- Provides your financial history when applying for credit, loans, or a mortgage

Plus, if you’re planning to build credit or apply for loans down the line, having a checking account is kind of the starting point for all that.

So, What Do You Need to Open One?

Here’s where it gets even easier. You don’t need to show up with a stack of papers. Most banks ask for a few standard documents:

- A government-issued ID (driver’s license, passport, state ID)

- Your Social Security number (or ITIN if you don’t have one)

- Proof of U.S. address (like a lease, utility bill, or even another bank statement) And if you’re opening the account online, you’ll just upload clear images of those documents.

- Additional documents like a Student ID or proof of enrollment for student accounts and documentation of all account holders in case of a joint account.

- Some banks might ask for an opening deposit—this can range from $0 to a couple hundred bucks depending on the bank.

What About Online vs. In-Person?

You can totally open a checking account online these days. Many folks prefer it to save time and avoid long queues.

But some people still like that face-to-face interaction—especially if they’re new to banking, want to ask questions, or just feel more comfortable handing over documents in-person.

Online banking usually comes with better digital tools, fewer fees, and a slicker app experience. In-person banking, on the other hand, gives you a physical location to walk into if anything goes sideways.

It really comes down to what you’re more comfortable with.

Individual or Joint Account?

Planning to manage the account solo? Easy—just open an individual one.

But maybe you’re opening it with a partner or a family member. In that case, you’d go with a joint account.

Both of you will need to provide documents and both will have equal access to funds. That’s great for shared expenses but does mean you’re both responsible for how that account is used.

So yeah—make sure there’s trust there.

Fees, Fine Print, and “Minimums”

A lot of accounts market themselves as “no or low-fee,” but sometimes that comes with conditions. Stuff like:

- You need to keep a certain balance

- You need to set up direct deposit

- You get charged if you use out-of-network ATMs

- Overdrafts & NFS can result in steep fees

- You may need to pay an inactivity fee if you stop using your account after 3–6 months. Some online accounts may charge a teller fee if you use a branch for deposits or withdrawal.

That’s why it’s worth reading the fine print or just asking someone at the bank directly. Most will walk you through it.

Getting Your Account Funded

Once your account is open, you’ll want to put some money in it.

Here’s how most folks do that:

- Transfer from another bank account

- Deposit a check

- Bring in cash (if you’re at a physical branch)

- Use a money order

Some banks let you do this instantly via mobile apps. Others take a day or two to process the initial deposit.

After that? Your debit card typically arrives in the mail within a week—or right on the spot if you’re opening in-person.

Managing It Like a Pro

Opening the account is step one. Using it well? That’s where you stay ahead.

Make sure you:

- Download the bank’s app and get familiar with it

- Set up transaction alerts (especially for low balances)

- Know where and how to access ATM networks

- Monitor your spending and income regularly

You’ll also want to understand some basics about banking codes—like the difference between routing and account numbers.

These show up when you’re doing transfers, setting up direct deposits, or paying bills online.

If you’ve ever wondered what is an account number or how it differs from a routing number, there’s a simple breakdown you can check out there. It clears things up fast.

A Note About Endorsements and Cash Flow

If you’re depositing checks into your account, you’ll also need to understand how to endorse them. Seems basic, but a wrong endorsement can delay your funds—or worse, cause rejection.

For a quick walk-through on who endorses a check and how to do it properly, take a look at that resource. Super helpful.

Wrapping Up

Opening a checking account in the U.S. isn’t some complex maze. You don’t need a finance degree, and you don’t need to guess your way through it.

Once you decide what kind of account works best for your life, find the bank that fits, gather your docs, and get started.

Make sure you read the details, understand the tools you’re given, and take a few minutes now and then to monitor things.

At the end of the day, this is your money—and your checking account is where that financial story begins.